Fix Cash Flow Fast: DSO Formula for Finance Leaders

Source: Pexels

Your team just closed a successful month. But if the cash hasn’t arrived in your account, you’re still stuck.

Sure, your revenue may look good on paper. But if your cash flow feels squeezed, the problem could be in your receivables.

Payments that take too long to arrive dry up your working capital. This delay slows down your operations and, of course, your growth. It puts pressure on your finance team to figure out how to cover the gap and keep your business running.

You can fix this problem by tracking one simple number: your Days Sales Outstanding (DSO). Simply put, it tells you how fast your business turns sales into cash.

This article will walk you through the DSO formula and explain how to use it. We’ll also show you how finance leaders use it to spot problems early and improve collections.

You’ll get real examples, clear steps, and tips to help you unlock faster cash flow.

Days Sales Outstanding (DSO) tells you how long it takes for you to collect money after you've made a sale. It measures the gap between when you send an invoice and when the cash arrives in your bank account.

For insurance businesses, DSO is a critical metric. A large part of your cash flow depends on how quickly you get paid by brokers, employers, or policyholders.

A high DSO means you’re waiting too long to collect. The longer that cash is stuck in receivables, the harder it is to cover claims. You also won’t be able to invest in operations or grow your business.

A lower DSO means you’re collecting faster. That gives you more flexibility, stronger financial health, and fewer surprises at month-end.

For finance leaders, DSO acts like a warning light. It helps you:

If you want a faster and more predictable cash flow, keep an eye on your DSO.

Think of DSO as your collection speed score. It uses two things you likely already have: your total accounts receivable and your total credit sales over a given period.

The basic formula:

You can calculate it monthly (30 days), quarterly (90 days), or annually (365 days). The number of days depends on how you track performance.

Let’s say your insurance agency had $600,000 in outstanding receivables at the end of the quarter. And your total credit sales over the last 90 days were $1.8 million.

Here’s how DSO would look:

Your DSO is 30 days. That means it takes you about a month, on average, to collect payment after a sale.

If your DSO started creeping up to 45 or 60 days, that could be a cause for concern. It could mean your receivables are slowing down and that your cash is taking longer to come in.

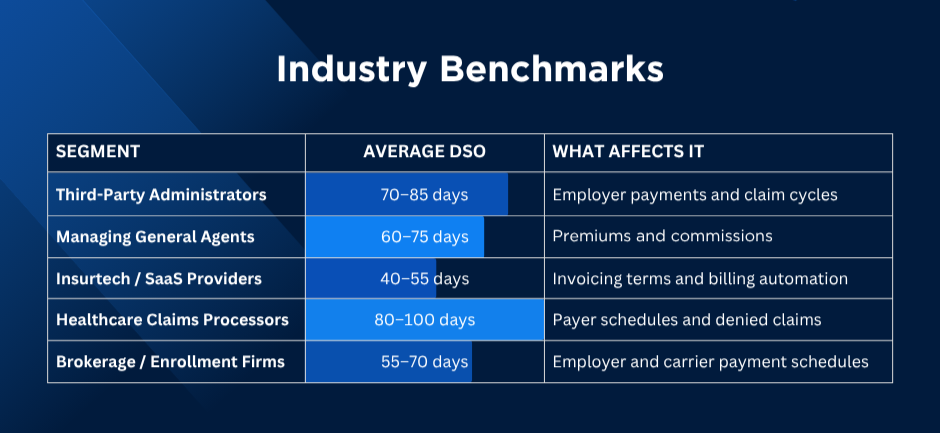

There's no single number that's considered a good DSO. To put this in more context, you need to know the current benchmarks in your industry. Here are the average DSO values for people in insurance:

What this shows is that even within the same industry, the average DSO still varies. It depends on how you bill, who pays you (direct customers vs. employer groups), and how often you follow up.

The goal is to keep your DSO within these values. Otherwise, you’re leaving cash on the table and slowing down your growth.

Your receivables are assets. But you can’t use them until they’re collected. A high DSO means your cash is stuck.

Suppose you’re a TPA billing $900,000 a month for claims admin services. With a DSO of 90 days, about $2.7 million is sitting in receivables at any time. That’s a whole lot of money you technically already earned but can’t use.

Now imagine you want to invest in automation to speed up compliance reporting. It costs around $250,000, but it could save your team hundreds of hours per year.

It's a great deal! But without the cash on hand, you may need to delay or borrow just to move forward.

Let’s say you take a short-term loan at a 9% annual percentage rate (APR).

Over 12 months, that loan would cost you roughly $22,500 in interest. That's thousands of dollars you'd have to spend just so you can access your money stuck in receivables.

A high DSO slows down your service and impacts your credibility with your partners. It holds you back from taking opportunities you’re otherwise ready for.

Reducing DSO isn’t only about collecting faster; it’s about fixing the underlying causes of delay. Top-performing finance teams improve cash flow by building smarter processes. They also use automation and tighten controls. Here's how they do it:

You can’t fix what you can’t see. So, the first thing you should do is get a clear view of your DSO.

Break down your receivables by payer type (employers, brokers, and carriers). Then, identify which segments are causing delays. Use this data to find patterns.

Who’s paying late? How often does it happen? Why are they taking too long to pay? Looking at this helps you better understand your DSO.

Remember to compare your current DSO to industry averages (and even your past DSOs). Doing so will help you get your bearings and find out where you stand.

If you can, track your DSO weekly and watch out for early warning signs. This enables you to address issues before they hurt your cash flow.

A weak credit policy invites payment delays. Make sure to review your terms regularly and adjust them based on client risk profiles.

For instance, you might want to:

It's important to communicate these expectations to your clients from the start. This way, they are more likely to accept your terms as a standard practice rather than view them as a penalty.

Source: Unsplash

Manual billing and paper invoices slow you down. To optimize the process, consider using e-invoicing tools. These automatically generate and send invoices with supporting documentation.

The sooner you send invoices, the sooner you can receive payments. And while you’re at it, make it easy for your clients to settle invoices.

Provide them with payment options like ACH or wire transfer. You may also consider online payment portals and offering auto-debit for recurring fees. You can even give them credit card options for smaller balances.

By doing so, you reduce friction and give your clients fewer reasons or excuses to delay payments.

Automation replaces repetitive manual work with consistent, error-free processes. For example, you can use accounts receivable (AR) automation tools to:

When paired with AR forecasting, you can also predict cash flow more accurately. These tools analyze payer behavior and payment patterns to help you manage your clients better.

Many businesses make the mistake of reacting to issues too late. With AR forecasting tools, you can spot problems early and act on them before they become bigger.

DSO gives a useful insight, but it doesn’t tell the full story. You need to add these complementary KPIs to your dashboard:

These show you if your improvements are real and driven by better operations. They also reveal if the changes are only due to seasonal trends. Looking at all these metrics gives you the full picture.

Sometimes, the problem lies in your operations. Delayed endorsement, missing documentation, or slow underwriting can stall an entire payment.

Work closely with claims, sales, and account management to clear internal blockers. Create standard operational procedures (SOPs) to flag and resolve these faster.

Improving DSO isn’t solely a finance issue. It’s easier to fix the problem if you align cross-functional teams toward the same goal.

Finance leaders resolve high-impact delays within hours by bringing all hands on deck.

Not all payer groups move at the same speed. National carriers have inherently longer cycles. Direct employers or brokers might be more responsive.

Set DSO goals per segment, such as client type or business line. This helps you focus your efforts where they matter most.

It's easier to improve cash flow when everyone works toward the same goals. Track progress across your teams and make DSO a shared key performance indicator (KPI).

To keep your teams motivated, make sure to celebrate your wins. Highlighting improvements reinforces the habits and processes that lead to faster collections.

Reducing DSO is a collective effort. Train account managers, customer success, and claims coordinators to support faster collections.

Teach client-facing teams to explain terms clearly. Show them how to spot early signs of payment risk. Loop them into follow-ups when needed.

Lowering DSO is the result of small, deliberate actions working together. It's how finance leaders create a faster and more predictable collection process.

Source: Unsplash

A mid-sized commercial insurance broker was struggling with slow payments. On average, clients took 78 days to settle their invoices.

The finance team sent invoices by hand and matched payments one by one. Collections dragged on, cash flow tightened, and growth plans stalled.

The finance team rolled out an automation platform. It linked their policy system, general ledger, and bank feeds.

With it, invoices went out the moment they bound a policy. Reminders ran automatically. The system matched bank transactions to invoices in seconds. It also flagged overdue accounts right away.

They added online payment options as well and gave small discounts for early payment.

In six months, they cut DSO from 78 to 52 days.

Cash on hand jumped 24%. This gave them room to fund marketing and hire new producers.

Collections work dropped by almost half. As such, the team had more time to focus on negotiating better carrier commissions.

Automation speeds up payments and operations. With the system doing the work for you, there's a lot less to worry about. It frees up valuable time so you can direct your efforts into growing your business.

More payment options and an easier process help clients pay on time. And when payments come in when they're supposed to, you get a better grasp of your cash flow. You can plan better and make decisions that move your business forward.

DSO measures how quickly you collect payments after a sale. A high DSO means cash takes longer to come in. This can limit your ability to pay bills or invest. Meanwhile, a low DSO maintains cash flow and keeps your operations running smoothly.

No, DSO cannot be negative. This is because it measures the average number of days it takes to collect payment after a sale. If customers pay in advance, that amount counts as deferred revenue, not a negative DSO.

High DSO can result from slow customer payments, unclear invoices, or weak follow-ups. It may also happen if your payment terms are too long.

If you want to optimize DSO, send invoices promptly and accurately. You should also follow up right away on overdue accounts and offer easy payment methods. Consider using automation to speed up collections and reduce payment delays.

Source: Unsplash

If you want to keep your business running, you need to keep your cash flowing. A healthy cash flow starts with understanding how long it takes for you to turn your sales into actual cash.

DSO is the way to go. By tracking this metric, you can turn collections from a bottleneck into a competitive advantage.

Start by understanding your numbers. Then, fix the processes slowing you down. It's also important to make DSO a shared priority across your teams.

The faster you collect, the stronger and more resilient your business will be.

The key is to simplify the process and offer fair payment terms. You'll also want to tap into automation that replaces manual work.

Lowering your DSO isn’t just about improving a number. It puts more cash in your hands, strengthens your finances, and gives you room to grow.

For finance leaders, that’s the kind of change that moves the business forward.

Take control of your cash flow today.

Our platform helps finance teams track DSO in real time, automate collections, and get paid sooner—without adding to your workload. Book a quick demo and see how easy it is to turn late payments into steady cash flow.