Balance Sheet Reconciliation: Step-by-Step Guide + Examples

If your balance sheet isn’t reconciled, it’s not reliable. Period.

A spreadsheet that balances doesn’t mean the numbers are right. Numbers can look neat in a report and still be wrong. What’s worse, they collapse the moment auditors take a closer look.

Reconciliation proves that your numbers can be trusted.

Many teams treat it like it’s optional, something to get to later if there’s time. That’s how small mistakes grow into bigger issues that take days to clean up.

This blog walks through what bank sheet reconciliation is and why it matters. We’ll also provide you with practical tips and examples that demonstrate exactly how the process works.

Table of Contents

So, What Exactly Is Balance Sheet Reconciliation?

Reconciliation means checking your balance sheet line by line. It confirms that every number matches official documents like bank statements. Any mismatches or gaps need to be tracked down and resolved.

Think of a balance sheet as the foundation of a house. If it’s uneven, every floor you build on top will tilt.

That’s what happens when balances don’t reconcile. One mistake at the base throws off every decision stacked on it.

Reconciliation isn’t there “just because.” It’s necessary to keep your records accurate and reliable. It’s also a safeguard against fraud and other issues that might harm your business.

Why Your Numbers Need Proof

Your numbers mean nothing without supporting evidence. Balance sheet reconciliation is precisely the proof you need. Here’s the actual value that reconciliation brings to the table:

- Accurate reports. Reconciliation ensures your reports reflect what actually happened in your accounts.

- Early fixes. It catches mistakes before they grow. This also lets you fix issues while they’re still easy to handle.

- Fraud check. It makes unusual or missing transactions easier to spot. Reconciliation flags irregularities that could signal fraud.

- Audit readiness. It keeps the proof behind every number, so audits run smoothly. With it, auditors can easily follow the money trail.

- Compliance. Reconciliation makes sure your reports meet accounting standards. Clean numbers mean your books can withstand scrutiny.

- Business confidence. Reconciliation fuels financial moves with trusted data. It lets you make decisions without second-guessing your numbers.

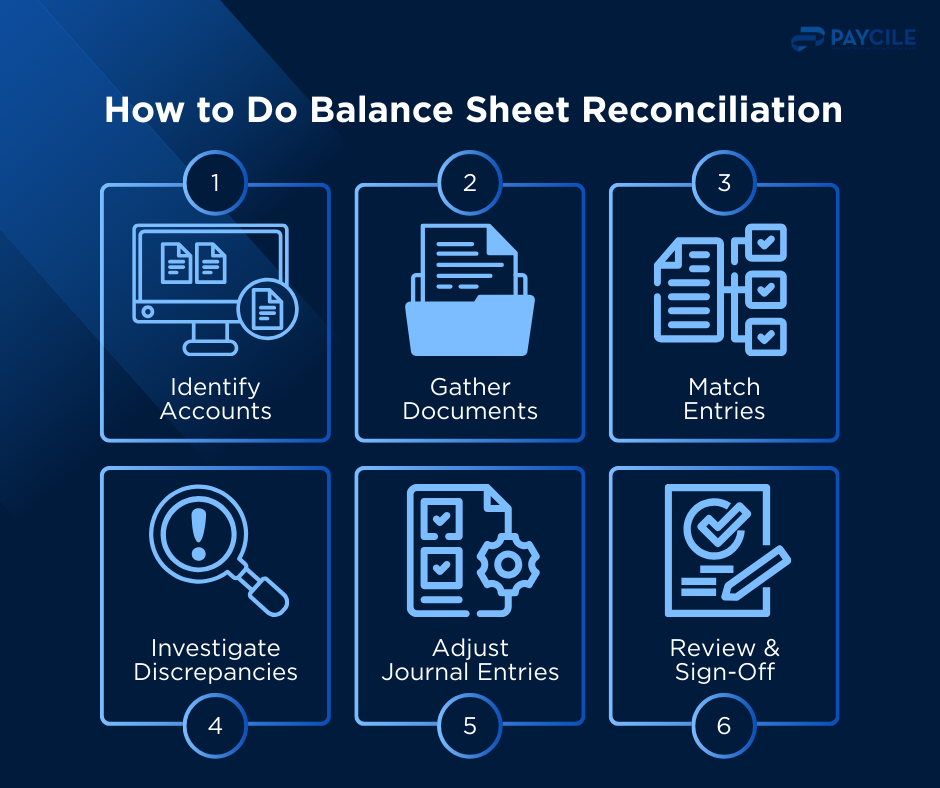

How to Do Balance Sheet Reconciliation Right

Reconciliation isn’t rocket science. But it does need a straightforward process. Here’s a step-by-step guide on how to do it right every time.

Step 1: Choose What to Reconcile

Pick which balance sheet accounts to review. Here are the most common accounts and the official sources they should line up with:

- Cash accounts — matched to bank statements

- Accounts receivable — matched to customer sub-ledgers

- Accounts payable — matched to vendor sub-ledgers

Other accounts include prepaid expenses, accrued liabilities, and fixed assets. By identifying accounts, you can focus on ensuring your most essential balances stay accurate.

Step 2: Round Up the Docs

Collect the proof behind each balance. Typical documents include bank statements, invoices, receipts, and sub-ledger reports. You’d also want to have on hand any schedules that track account activity.

Step 3: Match the Entries

Compare each balance to the supporting documents. Review each transaction to ensure the amounts and dates match.

Pay attention to timing differences. We’re referring to outstanding checks or payments that were cleared late. These can make your accounts look off at first glance.

Step 4: Track Down Mismatches

Find the source of any mismatch. Check for typos, missing transactions, or timing issues. It’s best to review your documents and trace each item until you find the cause of the mismatch.

Step 5: Correct the Books

Adjust journal entries to correct any mistakes. You also have to record missing transactions and update accruals and depreciation.

Be sure to document every change you make, so you can explain it if necessary.

Step 6: Double-Check Everything

Have a manager or controller check the reconciled accounts. This ensures accountability and accuracy. A proper sign-off also leaves a clear trail for audits and future reference.

What Reconciliation Looks Like in Real Life

Numbers don’t always match right away. Reconciliation is what catches those gaps and fixes them before they grow. The examples that follow demonstrate how this works.

Bank Account

Let’s say your general ledger shows a cash balance of $52,000. But your bank statement only shows $50,500.

At first glance, it looks like money has gone missing. However, upon closer review, you will see that the difference stems from a $1,500 check. It’s one you’ve already issued, but the bank hasn’t cleared it yet.

The money is already accounted for in your books, but it hasn’t yet been withdrawn from the bank account. The timing mismatch caused the difference in balances.

Reconciliation is necessary to bring both sides in sync. It’s the only way to confirm that your true available balance is $50,500.

Accounts Receivable

Suppose your ledger reports $200,000 in receivables, but the sub-ledger shows $198,000.

Where’s the missing $2,000? Did a payment get lost? Did you forget to record a transaction?

Through balance sheet reconciliation, you notice that an invoice was recorded in one system but entered late in another.

Once the transaction was posted, the balances matched at $200,000.

Fixed Assets

Your general ledger lists $150,000 in fixed assets. When compared to the asset register, the total comes to $145,500.

A closer look shows three minor discrepancies:

- You forgot to add a new printer → $2,000

- You sold a desk but didn’t remove it from the books → $1,500

- You didn’t record full depreciation for some computers → $1,000

After making these adjustments, both the ledger and the asset register match at $145,500.

Reconciliation confirms your balance sheet reflects the real value of what the company owns. This helps you avoid over- or under-reporting your assets.

The Usual Challenges in Balance Sheet Reconciliation

Reconciliation should confirm trust in the books. But more often than not, it’s where you realize your numbers aren’t as solid as they seem.

Here are the most common issues you may encounter in balance sheet reconciliation:

- Manual errors. A single typo can send an account off track. Missed transactions or wrong tagging only add to the mess.

- Timing issues. Payments clear on one side but not the other. Different periods, same transaction. Instant mismatch.

- Data silos. Bank statements, invoices, and ledgers sit in separate systems. Cross-checking transactions across these takes up valuable time.

- Resource strain. Closing drags when reconciliations take too long. The longer it takes, the less grasp you have on your cash flow.

- Audit stress. Missing documentation turns audits into chaos. Without backup, every number feels like a wobbly step.

These challenges don’t go away on their own. The only way around them is to become more informed about how reconciliation is conducted.

Smart Habits for Smoother Reconciliation

Reconciliation doesn’t have to be a nightmare. These small habits make the process faster and less stressful:

- Standardize the Process

Use clear templates and repeatable steps. A set process means anyone can replicate the task. It also leaves less room for mistakes.

- Reconcile Often

Don’t wait for the month-end. By reconciling more frequently, you can spot issues before they escalate. This also means less scrambling during monthly closes or audit season.

- Assign Responsibilities

Clear ownership prevents gaps and confusion. Create checklists and delegate tasks so that everyone is aware of what they’re accountable for.

- Use Technology

Automation speeds up matching. It also keeps documentation organized. With less manual work, there are fewer errors.

- Keep Audit Trails

Track every review and approval. Document all changes made in your accounts. With a clear trail, auditors have all the proof they need.

The Smarter Way to Reconcile

Even the best manual process has limits. Spreadsheets can’t keep pace when accounts and transactions multiply. That’s where automation changes the game. You achieve greater accuracy and faster closes without additional work on your part.

Automated matching

Forget combing through entries line by line. Automation matches transactions across ledgers, bank statements, and sub-systems. What used to take hours can now be finished in seconds.

Real-time visibility

Dashboards highlight unreconciled items as they happen. You can identify issues and take action promptly. This way, the month-end doesn’t leave you scrambling.

Error reduction

Manual entry leaves too much room for typos and missed records. Automation removes those weak points. It cuts down the errors that slow everything else down.

Audit readiness

Audit season becomes a lot less stressful with automation. Every step gets logged automatically. That means clear audit trails and complete documentation with minimal additional effort.

Faster closes

With automation, reconciliation runs in the background. As such, closing becomes faster and smoother. You also get to save resources and use them for more important tasks instead.

Closing the Books on This

Balance sheet reconciliation ensures that your financial statements accurately reflect reality (or a clear representation of it). That proof is what protects you from making bad decisions, dealing with messy audits, and incurring costly surprises.

The problem is that manual methods slow everything down. It takes up time your team should be spending on driving the business forward instead of tracking down mistakes.

Automation solves that by matching entries and flagging errors. Moreover, it maintains airtight audit trails in the background.

In short, you end up with numbers you can trust every time, without the grind. That’s why it has become the standard for finance teams that value accuracy and speed.

Let our tool do the work and keep your books spotless! Book a demo with us to see what it can look like for your team.