Embedded Finance Operations Without Rebuilding Your Platform

Embedded finance doesn't change your product nearly as much as it changes your responsibilities.

Once your platform starts moving money, you're no longer introducing a financial capability. You're operating one.

You're supporting financial operations that have to reconcile transactions, allocate funds, maintain accurate records, and keep multiple systems aligned long after a payment is complete.

Those responsibilities rarely make it into product launch announcements, yet they often determine whether embedded finance becomes a long-term advantage or an operational burden.

This article explores what embedded finance operations really involve, how they differ from customer-facing financial features, and how SaaS platforms can build the right operational foundation without rebuilding what already works.

Table of Contents

Embedded Finance Operations Are More Than Payment Processing

Much of the conversation around embedded payments centers on product capabilities.

Discussions typically focus on payment acceptance, lending, card issuance, or other financial services that customers can access without leaving a software platform.

Those capabilities are important because they're what users interact with every day.

Embedded finance operations begin after the transaction is initiated.

They encompass the operational processes that ensure money moves accurately through the business, financial records remain synchronized across systems, and every transaction can be traced from initiation through settlement and reporting.

While customers experience a seamless payment, finance and operations teams are responsible for ensuring the underlying financial activity remains accurate, auditable, and operationally consistent.

That distinction becomes more important as embedded finance for SaaS evolves from a product enhancement into a core business function.

Launching embedded payments doesn't simply introduce a new feature. It introduces an ongoing operational responsibility.

This is where many implementation discussions fall short. Technical integration is often treated as the primary milestone, while the operational infrastructure required to support that integration receives comparatively little attention.

Yet operational performance is what ultimately determines whether embedded finance scales efficiently or creates growing financial complexity over time.

For SaaS platforms, that operating model is no longer a back-office concern. It directly influences financial visibility, reporting accuracy, audit readiness, and the ability to introduce new payment experiences without increasing operational risk.

Understanding embedded payment operations through this broader lens changes the implementation conversation.

Instead of asking how to embed a financial feature, SaaS leaders can begin asking how to build an operational model that supports those features as the business grows.

That shift in perspective lays the foundation for every architectural decision that follows.

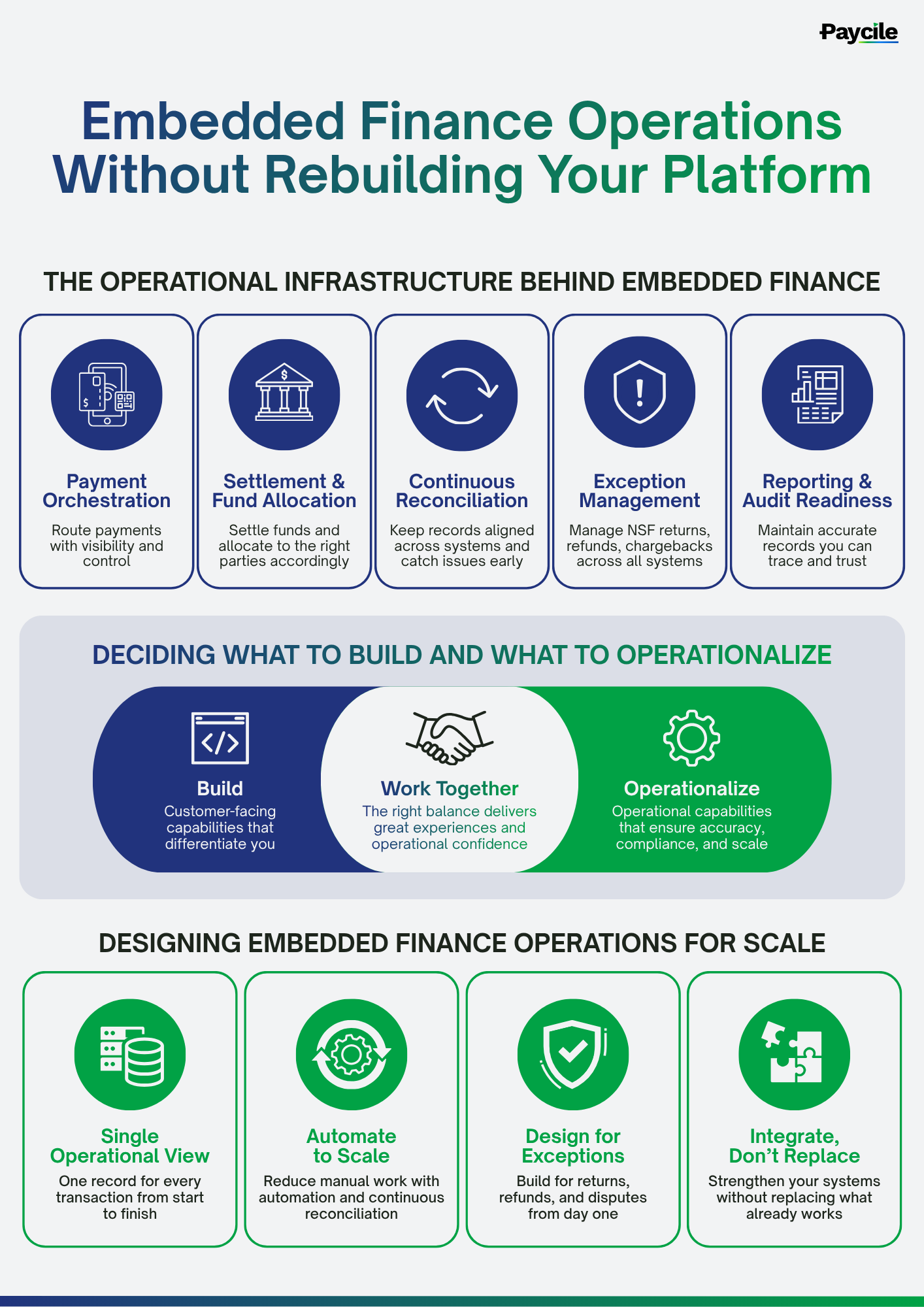

The Operational Infrastructure Behind Embedded Finance

Every payment introduces work that customers never see but businesses can't avoid.

Behind every successful transaction is a sequence of operational activities that determines whether financial data remains accurate, funds reach the correct recipients, and reporting reflects the true state of the business.

Each capability supports a different stage of the transaction lifecycle, but they function as a single operational system.

Payment Orchestration

Modern SaaS platforms often support multiple payment methods, providers, and transaction types.

Payment orchestration provides the visibility and coordination needed to manage those payment flows consistently while reducing operational friction as products and customer requirements evolve.

Settlement and Fund Allocation

Authorizing a payment doesn't complete the financial workflow. Funds still need to settle correctly and, in many business models, be distributed across multiple parties.

Marketplaces, property management platforms, and other vertical SaaS solutions frequently need to allocate payments between vendors, service providers, property owners, or platform accounts while accurately applying commissions, fees, or revenue-sharing arrangements.

Continuous Reconciliation

Financial information does not exist in a single system.

Payment processors, banking partners, internal ledgers, accounting software, and reporting platforms all maintain records that need to remain aligned throughout the transaction lifecycle.

Continuous reconciliation helps identify discrepancies as they occur, reducing manual investigation while improving confidence in financial reporting.

Exception Management

Not every payment follows the expected path.

Returns, refunds, chargebacks, and NSF transactions introduce operational changes that extend beyond reversing a payment.

They affect settlement, reporting, account balances, and financial records across multiple systems.

Managing these events consistently is essential for maintaining operational integrity as transaction volumes increase.

Reporting and Audit Readiness

Finance teams require reporting that reflects the complete transaction lifecycle, while auditors and stakeholders need confidence that every financial event can be traced and verified.

That level of visibility depends on maintaining accurate operational records from the moment a payment is initiated through its final financial outcome.

As transaction volumes grow and financial workflows become more complex, the strength of that foundation has a direct impact on efficiency, financial visibility, and the ability to expand embedded finance without increasing operational overhead.

Deciding What to Build and What to Operationalize

Every SaaS platform eventually has to decide which financial capabilities create competitive value and which are better supported by specialized operational infrastructure.

Customer-facing functionality often reflects the unique value of the software. Industry-specific workflows, user experience, business logic, and product differentiation are areas where internal engineering investment creates a lasting competitive advantage.

Product capabilities create competitive differentiation. Operational capabilities create consistency across the financial workflows supporting those products.

Recognizing that distinction helps determine where engineering investment delivers the greatest long-term value.

Building and maintaining payment orchestration, continuous reconciliation, settlement workflows, operational reporting, and exception management requires ongoing investment well beyond the initial implementation.

These capabilities evolve alongside payment methods, financial regulations, banking relationships, reporting requirements, and the broader SaaS payment infrastructure.

For many organizations, maintaining that operational layer eventually becomes its own engineering discipline.

That doesn't diminish its importance. Rather, it reinforces the need to treat operational infrastructure as a strategic architectural decision rather than an extension of product development.

Mature embedded finance architecture often reflects this separation of responsibilities.

The platform continues to own the customer experience and business logic that differentiate the product, while specialized operational infrastructure supports the financial workflows operating behind the scenes.

Instead of replacing existing systems, this approach extends them, allowing engineering teams to focus on innovation while finance teams gain greater operational consistency and visibility.

As the market continues to mature, the conversation is gradually shifting from customer-facing features to the infrastructure required to support them.

Recent embedded finance market analysis reflects growing investment in orchestration, workflow integration, and vertical SaaS infrastructure, reinforcing the shift toward specialized operational platforms.

Ultimately, the objective isn't to build less.

It's to own the capabilities that create strategic value while designing a transaction infrastructure that can scale alongside the business.

Designing Embedded Finance Operations for Scale

Operational models rarely fail because transaction volume increases. They fail because operational complexity grows faster than the systems supporting it.

Designing for scale begins with recognizing that operational complexity increases faster than transaction volume. The objective is to preserve financial accuracy, visibility, and reporting consistency as the business evolves.

Every Transaction Should Have One Operational Record

Every transaction should remain traceable throughout its lifecycle, giving finance teams a consistent operational record from initiation through final settlement.

Manual Processes Shouldn't Scale With Transaction Volume

As payment volumes grow, operational processes should become more predictable, not more dependent on manual intervention.

Automating reconciliation, payment matching, reporting, and exception workflows reduces operational variability while improving the reliability of financial information.

Payment Exceptions Belong in the Operating Model

Every payment ecosystem experiences refunds, returns, disputes, and other exceptions.

Scalable operations don't treat these events as edge cases. They incorporate them into the operational model from the outset.

This ensures financial records, reporting, and downstream workflows to remain consistent regardless of how a transaction concludes.

Integration Is More Scalable Than Replacement

Many organizations assume improving embedded finance infrastructure requires replacing accounting software, banking relationships, or internal financial systems.

In practice, scalability comes from strengthening the operational layer connecting those systems rather than replacing them.

An architecture built around integration allows organizations to preserve existing investments while improving operational visibility, financial consistency, and the ability to support future payment products without repeatedly redesigning their technology stack.

Designing for scale is ultimately less about preparing for higher transaction volumes than preparing for greater operational complexity.

The organizations that scale successfully are those that build operational models capable of adapting alongside the business rather than requiring continual architectural redesign as embedded finance evolves.

How to Evaluate an Embedded Finance Operations Platform

Choosing an embedded finance operations platform is less about comparing features than evaluating the operating model it enables. Several questions can help guide that assessment:

Can it support the entire transaction lifecycle?

Payment acceptance is only the beginning.

A platform should provide visibility from transaction initiation through settlement, reconciliation, reporting, and exception resolution.

Operational consistency depends on every stage remaining connected rather than functioning as separate workflows.

Will it strengthen existing operations or replace them?

Scalable embedded finance infrastructure should complement the systems an organization already relies on.

Look for solutions that integrate with existing accounting platforms, ERP systems, banking relationships, and internal products instead of requiring large-scale technology replacement.

The objective is to improve operational capability while preserving previous investments.

Can it adapt as the business evolves?

Operational requirements rarely remain static.

New payment methods, additional financial products, changing regulatory expectations, and expanding customer needs all influence how embedded finance operates over time.

The supporting infrastructure should be capable of evolving alongside those changes without requiring continual architectural redesign.

Does it improve operational confidence?

Perhaps the most important question is whether the platform increases confidence in financial operations.

Finance teams should have greater visibility into transaction activity, fewer manual processes, more reliable reporting, and stronger assurance that financial records remain consistent across the organization.

Those outcomes ultimately determine whether operational complexity grows alongside the business or remains manageable as embedded finance expands.

Evaluating an embedded finance operations platform through this broader operational lens shifts the conversation beyond implementation. It helps you establish a financial infrastructure capable of supporting those features as the business continues to scale.

Embedded Finance Starts With Features. It Succeeds Through Operations.

Launching embedded finance is only the beginning.

Sustaining it requires an operating model that can support increasing transaction volumes, financial complexity, and changing business requirements without sacrificing accuracy or visibility.

The long-term advantage doesn't come from offering more financial features. It comes from operating them with confidence.

See how Paycile helps SaaS platforms build embedded finance operations that scale.