Embedded Payments Reconciliation Explained: The Operational Layer Most SaaS Platforms Overlook

Embedded payments give customers one less reason to leave your product. What they don't do is eliminate the work that happens after the transaction.

Every payment still has to be settled, allocated, reported, and reconciled.

As payment volume grows, things get more complicated. Funds arrive on different timelines and payments get split across multiple parties. Refunds and chargebacks also create exceptions that need to be tracked.

For many platforms, reconciliation determines whether a payment program scales smoothly or creates ongoing friction.

This guide explains how embedded payments reconciliation works and why it becomes more challenging as volume increases. We also look into what teams should consider when building scalable payment operations.

Table of Contents

What Is Embedded Payments Reconciliation?

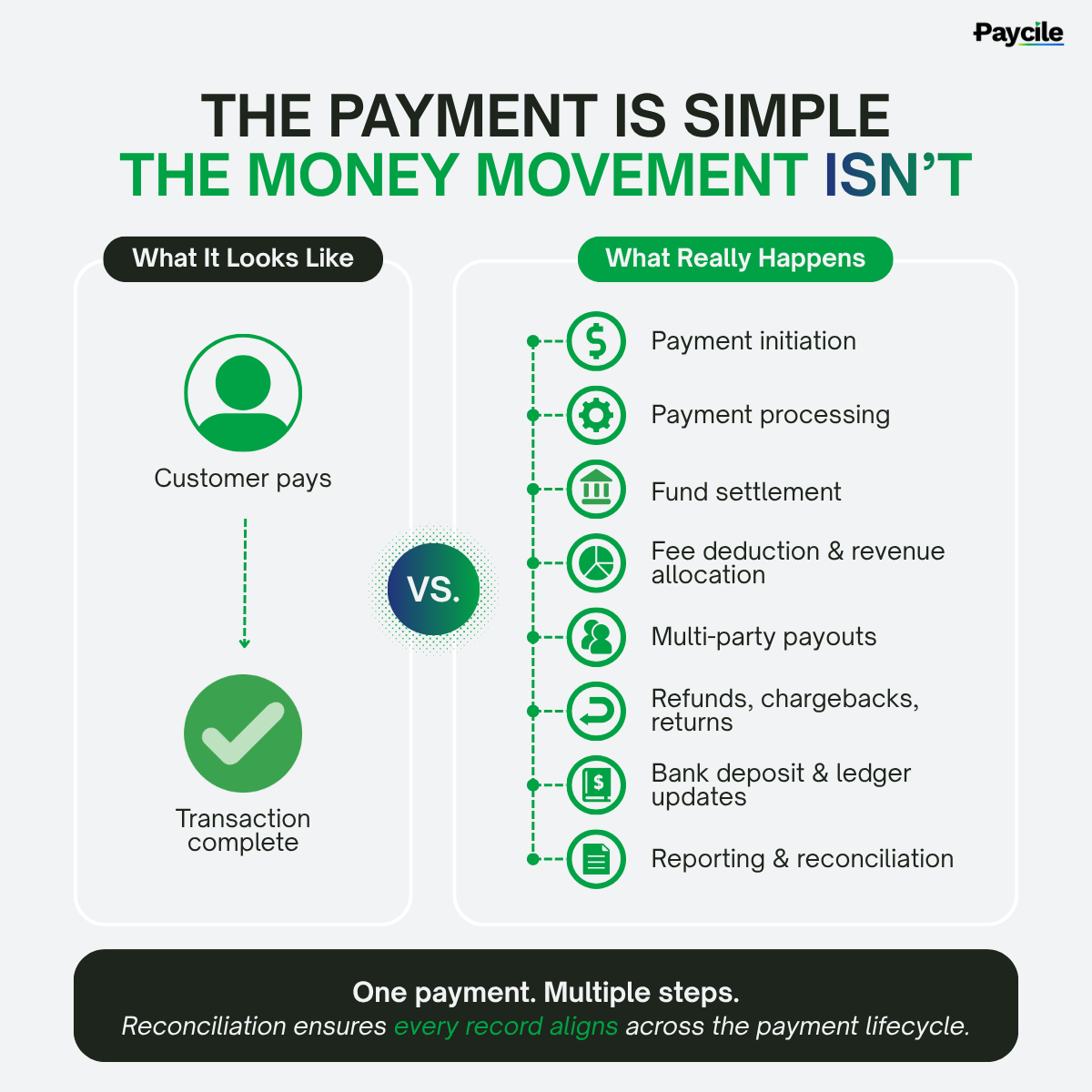

Embedded payments reconciliation is the process of matching payment activity that occurs inside a software platform with the financial records that ultimately reflect where the money moved.

Its purpose is straightforward. Every transaction should be traceable from initiation to settlement, with all supporting records aligned across processors, banks, ledgers, and accounting systems.

What Are Embedded Payments?

Embedded payments allow users to complete transactions directly within a software platform rather than leaving the application to pay through a separate portal.

For example, a tenant may log into a property management platform and pay rent directly through the resident portal. The payment experience happens entirely inside the software.

The same concept exists across HOA platforms, field service software, construction applications, healthcare platforms, and online marketplaces.

Embedded Payments vs. Integrated Payments

Although the terms are often used interchangeably, they are not identical.

Integrated payments connect software to an external payment provider. Embedded payments make payments part of the product experience itself.

From a financial operations perspective, both approaches require oversight. The difference is that embedded payments place more of the payment experience directly under the platform's umbrella.

Why Reconciliation Matters

A single payment transaction often generates records across multiple systems:

- The software platform records the transaction.

- The payment processor records authorization and settlement activity.

- Banks record deposits and withdrawals.

- Accounting systems record journal entries.

- Reporting tools generate financial summaries.

Each system may show a slightly different version of the same transaction. Reconciliation ensures those records ultimately agree.

Without it, teams lose visibility into cash movement and reporting becomes less reliable. Consequently, financial operations become increasingly difficult to manage.

Why Embedded Payments Make Reconciliation More Complex

As payments become part of the product experience, software providers take on greater operational responsibility.

Customers no longer view payments as a separate service. They expect the platform itself to provide accurate payment visibility, reporting, settlement information, and transaction history.

The payment itself may be handled by a processor, but it’s the platform that needs to explain where money went and how it moved.

That is where things get complicated. A simple payment on the surface often involves multiple systems, settlement events, fees, and fund movements behind the scenes.

Multiple Systems Create Multiple Sources of Truth

What often gets overlooked is the number of systems involved in a typical payment workflow.

A software platform may have its own transaction ledger. The payment processor maintains settlement records. Banks track deposits and withdrawals. Accounting platforms record financial activity. Reporting tools create summaries for finance teams and leadership.

Each system records information differently and updates on its own schedule.

When numbers don't match, finance teams have to determine whether they're looking at a real issue or a timing difference. The more transactions they process, the harder it becomes.

Settlement Timing Creates Visibility Gaps

Payment initiation and payment settlement rarely happen at the same time.

A customer may submit a payment today. The processor may settle funds tomorrow. The bank may post deposits a day later. Accounting systems may update according to a separate schedule.

A transaction can be progressing normally and still appear inconsistent across systems.

Without clear reconciliation processes, teams waste time chasing discrepancies that will resolve on their own.

Split Funding and Multi-Party Payments Increase Complexity

Many vertical SaaS platforms support payment flows involving multiple stakeholders:

- A property management platform may collect a rent payment that needs to be distributed between a property owner, management company, reserve account, and service providers.

- A marketplace may split funds between sellers, affiliates, and platform operators.

- A field service platform may distribute revenue between technicians, franchisees, and headquarters.

What appears to be one transaction often becomes several separate financial events.

Each distribution path must be tracked, verified, and reconciled. The more stakeholders involved, the more opportunities exist for mismatches and delays.

Payment Revenue Creates Additional Accounting Requirements

Embedded payments don't just move money. They also generate fees, revenue shares, reserves, and settlement adjustments that need to be tracked accurately.

That makes revenue recognition more complicated. The amount collected, the amount settled, and the amount ultimately earned are not always the same.

Finance teams need visibility into those movements to understand platform revenue, settlement activity, fee deductions, and where funds ultimately landed.

What Happens When Reconciliation Breaks Down?

The first sign of a reconciliation problem usually isn't a failed audit or a major reporting error. It's the growing amount of time spent investigating transactions that should have been easy to explain.

Teams build manual workarounds. Spreadsheets fill operational gaps. Individuals become responsible for tracking exceptions. Processes continue functioning until transaction volume reaches a point where manual intervention can no longer keep up.

When that happens, the consequences become difficult to ignore.

Cash Visibility Starts to Erode

Finance leaders operate best when they can trust the numbers in front of them. They need accurate answers to questions such as:

- How much cash is available?

- Which payments have settled?

- Which funds remain in transit?

- Which exceptions remain unresolved?

When reconciliation breaks down, even basic questions become harder to answer.

Teams are left piecing together information from processors, banking partners, internal ledgers, and reporting systems instead of working from a clear picture of payment activity.

Month-End Close Becomes More Difficult

Reconciliation issues tend to surface during month-end close.

Transactions that should match automatically require investigation. Exceptions accumulate. Reporting teams spend time validating balances instead of analyzing performance.

As a result, close processes take longer and finance teams devote more resources to transaction cleanup than strategic planning.

Audit and Compliance Risk Increases

Audits become a lot more difficult when teams can't easily explain how money moved through the system.

As payment volume grows, organizations need to show that transactions can be traced, settlements can be verified, and account balances can be supported by clear records.

That becomes especially important in industries where customer funds, trust accounts, or regulatory requirements are involved.

The issue is rarely a lack of data. More often, it's the effort required to piece that data together and prove everything reconciles the way it should.

Payment Exceptions Create Operational Drag

Tracking money movement is complex enough as it is. Reconciliation becomes a lot more challenging when previously completed transactions need to be reversed.

Refunds, chargebacks, and ACH returns don't just affect a single transaction. They can impact settlements, platform revenue, customer balances, and other downstream records that have already been processed.

By the time an exception occurs, funds may have already settled, reports may have already been generated, and balances may have already been reconciled.

Teams must then revisit those records, assess the impact across multiple systems, and determine what needs to be adjusted.

Every exception creates additional reconciliation work because multiple records need to be adjusted simultaneously.

Why Reconciliation Becomes an Operational Challenge at Scale

More transactions create more settlement events. More settlement events create more exceptions. More exceptions create more operational work.

Eventually, reconciliation becomes less about accounting and more about operational control.

Three-Way Trust Accounting Raises The Stakes

For some industries, reconciliation is not simply a reporting exercise but a compliance requirement.

Property management is a good example. Teams often need to keep bank balances, operator ledgers, and tenant ledgers aligned at all times.

When those records stop matching, the consequences extend beyond operational inefficiency. Organizations may face audit findings, compliance concerns, or regulatory scrutiny.

Discrepancies are not always obvious when they occur. A small mismatch can persist across multiple systems until someone notices it.

This makes resolution more time-consuming and increases the effort required to trace transactions back to their source.

Operational Visibility Matters More as Payment Programs Grow

As payment programs expand, tracking transaction activity across processors, banking partners, ledgers, and reporting systems becomes more complex.

What once felt straightforward can require significantly more effort to monitor and reconcile accurately.

Finance and payments teams often spend more time tracing activity across systems and validating balances. They also end up investigating discrepancies that become difficult to isolate at scale.

Visibility becomes particularly valuable during periods of rapid expansion, acquisitions, new product launches, or payment program changes.

Two payment programs can process similar transaction volumes and produce very different operational outcomes. The difference often comes down to visibility.

Manual Processes Become Harder to Sustain

At a certain scale, reconciliation can no longer depend on manual reviews and spreadsheets.

Organizations need systems capable of matching transactions automatically, identifying exceptions, and surfacing discrepancies before they impact reporting.

Most payment programs start with processes that work at today's volume. The challenge is ensuring those same processes still work as transaction volume grows.

When teams trust the numbers, they can make decisions faster and operate more efficiently.

What to Look For in an Embedded Payments Reconciliation Solution

When evaluating solutions, consider the following questions:

Can It Handle Multi-Party Payment Flows?

Look for support for split payments, revenue sharing, vendor disbursements, and other complex transaction structures.

Can It Connect Your Existing Systems?

Reconciliation gets difficult when payment data is spread across processors, banks, ledgers, and accounting platforms. The solution should bring those records together.

Can It Surface Exceptions Quickly?

Refunds, chargebacks, ACH returns, and settlement discrepancies should be easy to identify before they create larger reporting issues.

Does It Improve Operational Visibility?

Teams should be able to understand settlement activity, cash movement, and reconciliation status without relying on month-end reports.

Can It Scale Alongside Payment Growth?

The reconciliation process should remain reliable as transaction volume grows. What works today should still work when transaction volume doubles, triples, or increases tenfold.

As payment operations become more complex, the right reconciliation solution should do more than match transactions. It should help finance and payments teams maintain visibility as volume grows.

Embedded Payments Still Need Reconciliation

Embedding payments into a product can improve the customer experience and create new revenue opportunities. It does not eliminate the operational work required to support those payments.

As payment programs mature, teams need a clear understanding of where money moved, how it settled, and whether financial records remain aligned across systems.

Reconciliation plays a critical role in maintaining that visibility and ensuring confidence in the underlying data.

The platforms that scale embedded payments successfully are often the ones that invest as much in operational visibility as they do in payment infrastructure.

If you're evaluating how reconciliation fits into your embedded payments strategy, Paycile can help you explore the operational challenges, opportunities, and tradeoffs involved. Let’s connect!